The impact of infrastructure investment on real estate in Asia

Over the next decade, emerging Asia will invest around 5 to 6% of its GDP per year into infrastructure related projects. This translates into approximately USD 750 to 900 billion of new investment each year. Infrastructure investment has both short- and long-term benefits for a country's GDP as it helps to increase productivity, cut costs of economic interaction, and improve jobs as well as income levels, among other benefits.

The World Bank estimates that every 1% of GDP that is invested in a country's infrastructure stock goes along with an additional 1% increase in the GDP level.

By itself, this has a large positive impact on the real estate market, as prices tend to rise along with GDP growth, but more specifically this unique period of ample infrastructure investment offers opportunities for real estate investors to participate in the positive dynamics that follow such investment cycles. In this edition of Asia Insights we look into the specific benefits and opportunities for the real estate market that arise from infrastructure investments.

Much room for improvement

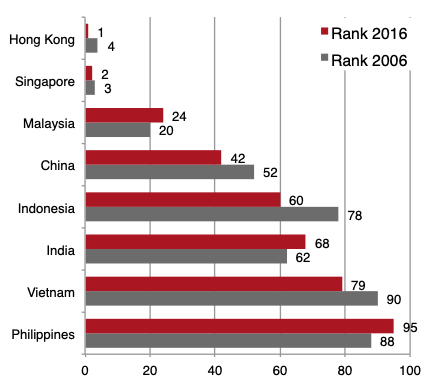

While infrastructure in the developed world is often very advanced, emerging Asia still has room for improvement. When looking at the yearly infrastructure ranking compiled by the World Economic Forum (WEF), China (#42), Indonesia (#60), Vietnam (#79), India (#68) and the Philippines (#95) all have ample room for further improvement.

Many Asian countries have invested heavily into infrastructure over the previous years and some countries made large leaps in improving their infrastructure as can be seen in the ranking. Over the past ten years China (+10 spots in the ranking), Indonesia (+18) and Vietnam (+11) improved significantly, while Hong Kong (+3) and Singapore (+1) even managed to occupy the two top positions. Meanwhile, India (-6), Malaysia (-4) and the Philippines (-7) lost a few positions, as their improvement was slower relative to other countries. However, in absolute terms, these countries also improved their infrastructure stock.

China has been leading infrastructure investment over several years with some of the largest infrastructure projects in the world such as the high-speed railway system or the hydroelectric three gorges dam. Other Asian emerging economies are following and are rapidly increasing their focus on intensifying infrastructure to catch up to the developed world and to help their economies to become more competitive and efficient.With role models like Singapore and Hong Kong close-by, they have access to the required knowledge and can learn from their experience.

Figure 1: Infrastructure Ranking over 10 years

The Indonesian government has made infrastructure a key priority and increased the budget in 2015 to 15% of total government spending from 10% previously. While the allocation of these funds was still slow after the budget increase, there were more projects started towards the end of 2015 and in 2016. For 2017, the government again increased the infrastructure budget by 22% to USD 30 billion. This represents almost 19% of the total state budget for 2017.

To facilitate investment the government has introduced multiple policies to speed up the overall process. One new policy facilitates land acquisition by the government for infrastructure projects that are of high public importance.

The government also actively supports projects on a top level. In October 2015, Indonesia and China signed a joint-venture agreement for the construction of a new high-speed railway between Jakarta and Bandung. The new line cuts down the travel time between the two cities to 35 minutes from currently three hours.

In the Philippines, government infrastructure spending gradually increased from just over 10% in 2011 to 14.9% in 2015. The government has proclaimed its term as the "golden age of infrastructure" and since the new administration took office in June this year, 17 large infrastructure projects have been launched, including a new 653 km railway link and an expansion of Manila's airport.

Similar developments are observed across the Asian region. From a real estate perspective, this poses the question how these large infrastructure investments will affect the real estate market and what opportunities will arise along the process.

What does it mean for the real estate market?

Infrastructure is generally subdivided into the categories energy, transportation, water, and telecom, as well as social infrastructure, which includes healthcare and educational facilities.

The positive contribution of infrastructure development to long-term growth is well documented. Besides the estimate from the World Bank, a recent study from the Federal Reserve Bank of San Francisco conducted in the US finds a GDP multiplier of 2 or more for road infrastructure investments, i.e. an increase of at least two additional GDP dollars for each dollar of investment. Different studies conclude in a multiplier effect of 0.5 to 1.5 depending on where the study was conducted and what kind of infrastructure investment was investigated.

With better infrastructure it becomes easier to do business as the cost of communication, transportation, sanitation, and energy decreases. Businesses and people can operate more efficiently, and are more competitive among peers.

Also, people live healthier in this improved environment and can contribute better to society. The studies highlight, however, that investment must be allocated effectively to have a long-term positive impact on GDP.

In our previous Asia Insights, we have highlighted the close relationship between GDP levels and real estate prices. As an economy becomes wealthier, real estate prices tend to rise. Infrastructure investment thus affects the real estate market on a broad basis.

Secondly, it directly affects projects in the proximity of the infrastructure investments.

The effect is mainly associated with the improvement of transportation infrastructure as the accessibility is of essential importance to every real estate asset.

The industry credo "location, location, location" is rooted to a large extent in convenient access to transportation infrastructure such as buses, metro or train stations, airports and highways.

The transit premium

Multiple studies indicate that a large positive effect on real estate is associated with high-capacity transit stops, such as metro or light rail stations. While a nearby airport can have a positive effect on commercial and office space, it can be negative for residential space due to negative externalities such as airplane noise.

Higher property values near transportation infrastructure are a phenomenon known as the "transit premium". A literature review done by the US based Center for Transit Oriented Development (CTOD) finds that transit premiums range from a few percent up to over 150%. For office, premiums range from 9% to 15%, for retail from 1% to 167%. For residential properties, single-family dwellings had a premium range of 2% to 32% and for condominiums from 2% to 18%.

A study by Knight Frank Residential Research looked at residential property prices in short walking distance to the future crossrail stations in London. Crossrail is a large addition to London's public transportation network increasing the capacity by 10% and substantially cutting down travel times within the city. The project was officially approved in 2008 and the first stage will be completed in 2018.

Between 2008 and 2015, residential prices within a 10-minute walking radius around the planned stations experienced a price growth of 57%, compared to 43% in the prime central London market. A further price hike is expected closer to the opening of the first line in December 2018.

Further researchers find that locations near transit exhibit less volatility in a market downturn, as prices tend to be more resilient. The transit premium is explained by multiple factors. On commercial centers, transit centers have a positive impact because they generate large people flow. This increases the likelihood that people see advertisements or services, and may eventually purchase something. For offices, being close to transit centers add a lot of convenience for the tenants' employees and clients. Residents living or working near a transit center enjoy better connectivity to other parts of the city within a shorter time frame.

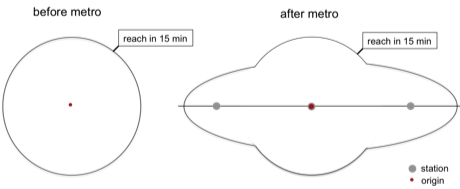

The enlargement of the area that can be reached within 15 minutes – thanks to a new metro stop – from a given location is illustrated in figure 2.

Figure 2: A new transit stop increases the area that can be reached within a given time frame

Within a given time frame, a person can travel further than before and also reach more points of interest. The location thus becomes more desirable. New and upgraded transit stops translate into opportunities for investors as locations in proximity to these become more attractive as well. Also, these locations provide opportunities to build commercial uses at potentially higher density.

Asia's commitment to public transportation

Today, Asia is the world's region that invests most in infrastructure. Shanghai and Beijing already have the worldwide largest public transportation systems. Shanghai's metro network is the longest and consists of 588 km of track. Beijing follows suit with 554 km. Both cities continue to extend their networks each year with new lines or extensions.

Jakarta is currently building its first metro line that connects the populous south to the city center. The line is expected to be operational in 2018 and will transport 173'000 people a day, considerably easing the pressures on the road network.

Further, the city is building a new light rail network system throughout the city that will connect the suburban areas around the city. The first phase of this project will encompass 42 km of track, with plans to extend to 130 km over the coming years.

With the launch of the 2018 Asian Games in Jakarta, the city is rapidly ramping up its transportation capabilities and is determined to complete in time for the event.

Ho Chi Minh City, the largest city in Vietnam, is currently building the first two lines of its metro system with the first line scheduled for completion in 2020. The city plans a total of six lines with a total network size of 107 km.

Bangkok just opened its second metro line, and has approved the construction of three more lines. Other cities such as Manila in the Philippines, Guiyang in China or Hanoi in Vietnam have similar plans to upgrade or build such infrastructure.

As new transit stops emerge, they profoundly shape the real estate market around the area. Higher density is often encouraged to effectively use the better accessible land area, and commercial space becomes more sought after as more people pass through the area. Along with other infrastructure improvements such as rail networks, highways, new and upgraded airports, Asian cities are on a positive track to spur further growth and welfare.

While ambitions are high the key will be successful implementation of large-scale projects. Shanghai, Singapore, Hong Kong and Beijing lead the way for other cities to follow.

Figure 3: Future and current public transportation infrastructure in AsiaEnter heading here...

Implications for investors

Infrastructure is a key consideration for every real estate investment. The ongoing upgrade of Asia's infrastructure has a profound impact on the market both in terms of broader GDP and value growth as well as an upgrade of specific locations due to new transportation infrastructure such as new metro and light rail lines. New opportunities for real estate development can arise from such infrastructure, and property in vicinity of public transport becomes more attractive. The concept of the transit premium helps to explain these price developments. Investors must, however, be prudent not to anticipate too high of a transit premium stemming from future infrastructure developments. Proper due diligence and market research comparing the prices around future and existing transit stops to more remote areas help to assess arising opportunities. With infrastructure investment happening on a broad scale and with strong implications for growth, the Asian real estate market will continue to benefit from this development.

Sources

ADB; asean.org; Bloomberg; CB Richard Ellis; China Daily; CEIC; Centaline; CitiBank; Colliers International; Credit Suisse Research; Cushman & Wakefield; Deloitte; Diener Syz Real Estate; DTZ Research; Economist Intelligence Unit; Financial Times; Franklin Templeton; Frost and Sullivan; GaveKal Dragonomics; IMF; institute for building efficiency; Jakarta Post; Jones Lang LaSalle; Knight Frank Research; KPMG; LaSalle Investment Management; McKinsey Global Institute; Morgan Stanley Research; National, Provincial, and Municipal Bureaus of Statistics; Nomura Research; OECD; People's Bank of China; Political & Economic Risk Consultancy Ltd; PricewaterhouseCoopers; Reuters Real Estate; Savills; Shanghai Daily; Thomson Reuters; Trading Economics; UBS Research; UN; Wall Street Journal; WTO; World Bank; World Energy Outlook (IAE); Xinhuanet

Our complimentary publications inform you about current developments in the Asian real estate market and key trends in the real estate industry. Sign up to receive them automatically.