Global real estate portfolios and local currencies – to hedge, or not to hedge

To hedge, or not to hedge? Although the question is not quite as dramatic as Prince Hamlet's in Shakespeare's masterpiece, it is still a relevant question for any global real estate investor, especially during times when the global financial markets are turbulent and volatility is spiking.

Home bias versus international diversification

A large-scale study by Morgan Stanley Capital International (MSCI) has shown that on average 83% of real estate investments are made in their home market (MSCI, 2018). The 2019 edition of the Swisscanto Pension Fund Study also confirmed this phenomenon in Switzerland: Swiss pension funds have invested an average of 24.8% of their assets in real estate, a mere 10% of which is allocated in various markets outside of Switzerland (Swisscanto, 2019).

However, this evident home bias is increasingly eroding, as property prices in the developed world have risen substantially and yields have consequently been compressed over the past decade. Interest rates near zero and the lack of investment alternatives will not change the current low-yield environment any time soon, pushing real estate investors to look for yields beyond their home markets. In addition to exciting opportunities and attractive investment returns, a globally allocated real estate portfolio also provides a substantial diversification effect.

By adjusting their geographical asset allocation, investors are automatically adding foreign currency exposure to their portfolios and are facing the question whether to hedge or not to hedge the corresponding risk.

This Asia Insights provides a closer look at foreign currency exposure that arises in connection with an internationally diversified real estate portfolio. The paper also examines the benefits of a natural hedge and whether hedging currency risks is effective for long-term investments.

Foreign currency exposure

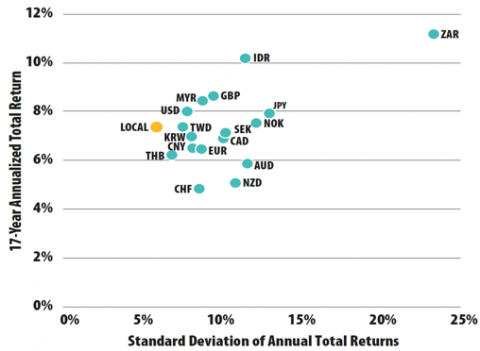

Fluctuations in the currency markets can have a substantial impact on an international real estate portfolio value and the rental yields of the underlying properties. The MSCI IPD Global Annual Property Index illustrates the effect of foreign currency exposure on historical performance between 2001 and 2017.

The MSCI IPD Global Annual Property Index is a valuation-based index, so the standard deviation should not be interpreted as a true risk estimate, but it can still provide an indication of how variable returns were over a time period.

As Figure 1 shows, the relationship between risk and return varies substantially depending on the reporting currency. Over the full 17-year history of the index, the annualized total return in local currency (i.e. fully hedged without currency impacts) has been 7.4%, and the standard deviation on the annual total return was 5.8%. Calculating the index in other currencies shows just how different the unhedged performance of that index would have looked to investors in different parts of the world.

Figure 1: Performance and reporting currency

For example, measured in the Indonesian Rupiah (IDR), the index would have returned 10.2% with a standard deviation of 11.8%. From the perspective of a Swiss franc (CHF) oriented investor, the index would have returned 4.9% with an 8.5% standard deviation. The large difference in performance illustrates the substantial impact that currencies can have. While Figure 1 highlights how much the currency effect has been in the past, investors may face even higher currency risks in the future. Recent MSCI research found that, in the aftermath of the global financial crisis, foreign currency risks were rising as a combination of quantitative easing, currency wars, and political uncertainty made currencies more volatile.

As in other asset classes, real estate related foreign currency risks can be divided into three basic categories: transaction risks, translation risks and economic risks.

Transaction risks arise when cash flows are converted from one currency to another. For example, transaction-related risks often arise when buying or selling a property and when repatriating rental income. These risks can be reduced if, for example, the purchase price is paid in instalments or the timing of the repatriation of rental income is flexibly arranged.

Translation risks arise when assets or liabilities in a foreign currency have to be converted into the accounting currency. This is an accounting evaluation that takes place regularly on certain valuation dates at the end of each accounting period and therefore conversion timing is not flexible.

Economic (or operating) risks are lesser-known than the two risk types mentioned above, but are nevertheless a significant risk. Economic exposure is a measure of the change in the net present value of a company or an asset as a result of fluctuations in cash flows caused by changes in foreign exchange rates. Increasing globalization and economic relations between countries have made economic exposure a source of risk almost for all market participants. Since unanticipated rate changes affect a company's cash flows, economic exposure can result in negative consequences for a company's operation and profitability. A stronger foreign currency will make foreign production more expensive, while profits earned in foreign currencies will decrease. Furthermore, economic exposure can undermine a company's competitive position. For example, if the local currency strengthens, local manufacturers will face more intense competition from foreign manufacturers whose products will become cheaper. This type of exposure cannot be easily mitigated because it is related to the unpredictable fluctuations of currency exchange rates.

Global real estate investors are mostly affected by transaction risks due to the nature of the asset class and the regular rental income, while translation and economic risks impact real estate to a lesser degree.

Optimal hedge ratio

Transaction and translation risks can be hedged using different instruments: forwards, futures, swaps and options are typically used to mitigate such risks.

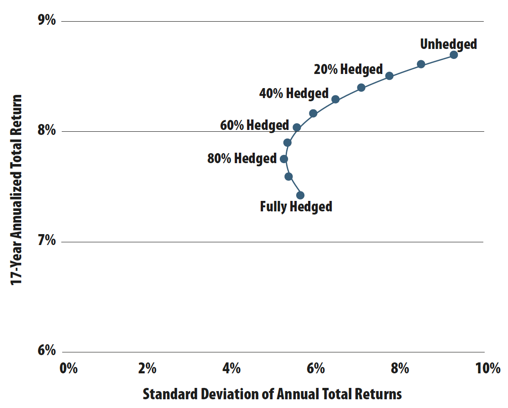

When hedging, an investor needs to decide on the hedge ratio: how much of the total exposure shall be hedged. Even if a 100% currency hedge seems attractive at first glance, various studies have shown that this was not efficient in the past. Figure 2 illustrates the risk-return tradeoff for portfolios with different hedge ratios along the efficient frontier from 2001 to 2017. The maximum return was achieved without hedging any currency risks, and the global minimum-variance portfolio was achieved with an 80% hedge rather than a full hedge. In addition, Figure 2 shows that a fully hedged portfolio was not efficient either from a total return or a standard deviation perspective.

Figure 2: Effect of different hedge ratios on total return and standard deviation

Diversification benefits

In principle, as explained above, it is not possible to fully hedge against economic risks. However, a global real estate investor with a broadly invested portfolio can benefit from substantial diversification effect. If, for example, a global real estate portfolio is being analyzed, the following effects are reducing the overall portfolio risks.

There is a high probability that real estate cycles of different countries will be diverse. Within a single country, it is also possible that different sectors will develop in different directions which can provide additional diversification. A globally diversified portfolio can effectively balance out the performances of the various economies and real estate sectors. In addition, multiple investment currencies also help to smooth out the effects on the reporting currency.

All in all, the diversification effect helps to reduce country or currency specific risks and to achieve an optimized risk/return profile.

Natural hedge

In addition to the above-mentioned diversification effect, a global real estate investor with a broadly diversified portfolio benefits from a so-called natural hedge.

It can be assumed that real assets offer a natural hedge compared to nominal assets. In order to be able to analyze this topic in more detail, various macroeconomic relationships have to be examined.

First, the connection between inflation and nominal assets. Nominal investments, such as cash, money market instruments or bonds, do not offer protection against inflation. To derive the real return of an asset, inflation must be deducted from the nominal interest rate. If inflation is higher than the nominal rate, investors are facing negative real returns and are losing money in terms of purchasing power. If inflation is lower than the nominal rate, the real yield is still positive but reduced by the amount of inflation.

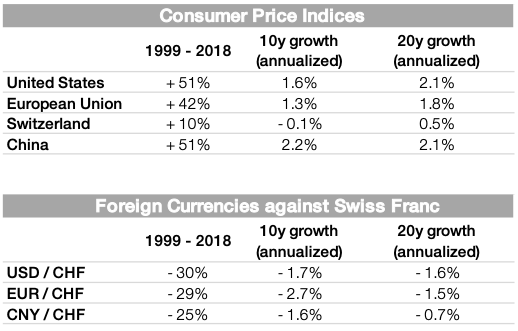

Table 1: Relation between CPI and exchange rates

Second, the relationship between inflation and real assets. In contrast to nominal assets, real assets, such as equities or real estate, offer so-called inflation protection. Increasing consumer prices will lead to a higher overall inflation in the respective country. Real assets like real estate will benefit from this development with simultaneously rising property prices and thus protection against losses in real value due to inflation.

Finally, and most importantly for international real estate investors, the link between foreign exchange rates and inflation. Table 1 below shows a strong link between Consumer Price Indices (CPI) and foreign currency exchange rates against the Swiss Franc, which experienced the by far lowest inflation. Basically, rising consumer prices are compensating investors if a local currency depreciates against other currencies.

China's consumer prices, as an illustrative example, increased by 51% over the 20-year period and the development of the CPI was comparable to those in the United States and Europe. At the same time, the Chinese Renminbi did not depreciate against the U.S. Dollar or the Euro but actually even strengthened a bit.

A comparison with Switzerland shows a different situation. The Chinese currency weakened against the Swiss Franc over time and lost 25% in value within the last 20 years. But investors got compensated in real terms since the Chinese CPI grew substantially more than consumer prices in Switzerland between 1999 and 2018.

History has constantly shown that there is a relation between Consumer Price Indices and foreign currency exchange rates. As Table 1 illustrates, a weakening currency is naturally accompanied by rising consumer prices, and rising real estate values along with it.

How are investors in Asian real estate markets affected by the above-mentioned link between foreign exchange rate and inflation? Table 2 illustrates the relation between multiple macroeconomic figures and the effective real estate price growth for a Swiss Franc denominated investor.

First, high nominal GDP growth rates were accompanied by strong real estate price growth in local currencies. China for example has high nominal (10.9% p.a.) as well as real (7.8% p.a.) GDP growth rates which led to a substantial real estate price growth (7.7% p.a.) over the last years. In comparison, with more moderate GDP growth rates, Singapore's nominal real estate price growth was lower than that in China.

Table 2: Effect of GDP growth, inflation rate and currency impacts for CHF denominated investors

Second, as Table 1 has shown, countries with weaker currencies against foreign currencies are generally showing higher inflation rates. The Indonesian Rupiah depreciated on average 3.0% per year against the Swiss Franc. Over the same period, Indonesia had a high average inflation rate of 4.7%. Indonesia's real estate price inflation compensated for its Rupiah's loss.

Third, investors are achieving attractive returns in their denomination currency. Let's assume an investor has an equally balanced real estate portfolio across all five countries mentioned in Table 2. Although Swiss investors were faced with an average currency loss of 1.7% per year due to a strong Swiss Franc, they were compensated by an average real estate price growth in Swiss Franc of 5.8% per annum.

Therefore, real estate investors can expect a weaker currency to be compensated by a higher inflation rate and thus rising consumer prices as well as real asset prices. In markets with high GDP growth, the rise in real asset prices typically overcompensates the loss in a depreciating currency. Investors hence benefit from a natural hedge from real assets such as real estate.

Implications for investors

In principle, investors must conduct cost-benefit analyses and decide whether foreign currency risks should be hedged or not. In addition, investors need to answer the question as to which asset classes and what share of their portfolios should be hedged.

In sum, there are strong economic reasons that speak against hedging real estate holdings with a long-term investment horizon:

- First, hedging foreign currency positions over a long period can be very costly due to interest rate differentials and transaction costs, especially when hedging high-yielding currencies from a low-yielding environment. The overall situation for investors gets worse when hedging a currency with positive real returns to a currency with negative real returns due to the additional drag by the inflation difference.

- Second, a hedge and even diversification benefits also emerge for investors with globally diversified real estate portfolios as they navigate through the economic cycles of their various investment destinations. Underperformance in one country or one sector can be effectively offset by overperformance in another.

- Finally, there is a strong link between consumer prices and foreign currency rates: rising consumer prices compensate for depreciating currency values. Also, real estate prices rise in tandem with inflation and consumer prices. Thus, if currency depreciates and inflation increases, real estate prices will grow to offset currency losses, offering a so-called natural hedge.

All in all, investors will need to balance pros and cons of hedging foreign currency risks and answer the question for themselves whether to hedge or not to hedge.

Sources

MSCI, Swisscanto, MSCI Global Intel PLUS, OECD, Bloomberg, World Bank, The Fed, OECD, BIS, Asia Green Real Estate

Disclaimer

© 2020 Asia Green Real Estate AG, Switzerland. No warranty can be accepted regarding the correctness, accuracy, uptodateness, reliability and completeness of the content of this document. Asia Green Real Estate expressly reserves the right to change, to delete or temporarily not to publish the contents wholly or partly at any time and without giving notice. This document as well as its parts is protected by copyright, and it is not permissible to copy them without prior written consent from Asia Green Real Estate. This material does not take into consideration the specific investment objectives, financial situation or particular needs of any person that enters into a relationship with Asia Green Real Estate. No representation or warranty, expressed or implied, is made by Asia Green Real Estate regarding future performance. This material is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of, or located in, any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or subject Asia Green Real Estate to any registration requirement. The document may contain forward-looking statements that reflect Asia Green Real Estate's current views with respect to, among other things, future events and financial performance. Any forward-looking statement contained in this material is based on our current estimates and expectations and are subject to various risks and uncertainties.

Our complimentary publications inform you about current developments in the Asian real estate market and key trends in the real estate industry. Sign up to receive them automatically.