Proptech startups - reshaping the rental housing market in Southeast Asia

Technology has shifted the way people live and work, creating new opportunities for business and driving the economic growth. Twelve disruptive technologies are believed to bring significant economic impacts by 2025 (McKinsey Global Institute, 2013), whereof mobile internet is deemed to imply the largest disruption by allowing for service delivery improvement, productivity rise, and time efficiency which ultimately creates a value of convenience. In the property industry, any technology utilized for real estate spaces is called Proptech, an abbreviation for Property Technology. With a total of USD 7.8 billion invested in their startups worldwide from 2013 to mid 2017 (Graph 1), Proptech is no longer a niche phenomenon (Jones Lang LaSalle, 2018).

Disruptions of strong Proptech startup like Airbnb are evident in the United States and Europe. It has been estimated that in Austin, where Airbnb supply is highest, the causal impact on traditional hotel revenue is in the range of 8%-10% (Zervas et al., 2017). In Florence, Italy, almost 20% of the entire housing stock is listed on Airbnb, emptying the historic Italian city from long-term tenancies (University of Siena, 2017).

Local authorities and residents were worried that such Proptech startups are pushing up rents. In anticipation of an unaffordable rental housing market, short-term rental restrictions were adopted in the world's most-visited cities namely Amsterdam, Barcelona, Berlin, London, Palma, New York City, Paris, and San Francisco. Restrictions include limiting the number of days in a year for short-term rentals and requiring landlords to obtain certain permits or licenses for renting out their properties (New York Times, 2018).

While the Proptech sector appeared in the past few years in Western markets on account of technology, the next movement of property management transformation is likely to take place in Asia. It has been reported that during 2013 to mid 2017, 179 startups in Asia Pacific have gained US$4.8 billion or over 60% of the total Proptech investments – with China and Hong Kong contributing US$3 billion of that amount (CB Insights, 2017). Southeast Asia's Proptech sector is, on the other hand, notably younger if compared to China – including Hong Kong – and India.

Graph 1. Proptech financing by regions

Nevertheless, Southeast Asia is rapidly catching up with dynamic new Proptech firms. The number of internet users in the region is expected to grow to 480 million by 2020 from 260 million in 2018. Moreover, Google and Temasek Holdings projected online advertising spending to increase from USD 2.1 billion in 2015 to USD 9.9 billion in 2025 (Google & Temasek, 2016).

This ASIA INSIGHTS will further explore the new wave of Proptech startups in Southeast Asia and the implications on the rental housing market. The Southeast Asian countries mentioned in this article are Indonesia, Malaysia, Singapore, Philippines, Thailand, Vietnam, and Sri Lanka.

What is proptech and how does it work?

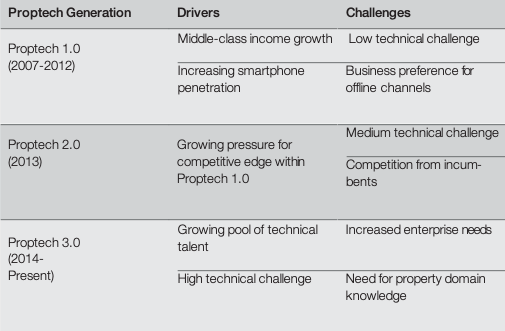

Proptech, or Property Technology, was initially linked with the facilitation of three different property activities including information provision, transactions, and management and control on the strength of the internet (University of Oxford, 2017). The internet enables users to obtain property-related news and advices, while providing online marketplaces for real estate transactions both for sales and letting, and allowing building systems to be controlled remotely.Proptech is also defined as "the utilization of technology as a solution to challenges in the real estate sector" (Jones Lang LaSalle, 2018). It entered the UK and US real estate industry since the mid-1980s with the invention of a PC-driven property research tool, mainly utilized for organizing and analyzing data describing the performance of a commercial property. However, it has not been until 2007 that Proptech has arrived in Asia Pacific with the launching of a property-listing site. Today, Proptech startups have evolved into more advanced platforms, as outlined in Table 1.

Proptech 1.0 began with the middle-class population and income growth stimulating more demand for homes. Alongside with increasing smartphone usage, home buyers started to utilize the internet for property searches. A Singaporean startup, PropertyGuru, came up in 2007 to address consumers' need for a single online portal offering different listings. With a direct-to-consumer or pay-to-list business model, such marketplaces pose relatively low degree in technical challenge.

Proptech 2.0 arose in the response to the needs of small brokers and businesses that are rather more complicated than the consumers themselves. New waves of commercial property intelligence platforms arrived in 2013, providing tools that can improve business processes and decision-making.

Table 1. Evolution of proptech in Asia Pacific

At this stage, tech talents availability was growing, thus, startups were able to equip their platforms with more advanced technologies like data analytics and virtual reality, while using a pay-to-use or software subscription business model.

The current Proptech 3.0 wave emerged in 2014 where startups employed drones for both marketing purposes and remotely conducted building inspections, giving added values to real estate agents, developers, and tenants. A number of Proptech startups offering smart home devices that are easily accessible through the internet are expected in the coming years. Such innovations are built to address increasingly complex needs.

New waves of proptech startups in Southeast Asia

OYO Rooms – OYO Rooms is a Proptech startup providing room operations and management services for independent property owners and hoteliers. Over the past few years, a growing number of Indian millennials were observed renting new homes because they move away from their hometowns and shift to new cities to access job opportunities (Entrepreneur India, 2018). The founder of OYO Rooms sensed this opportunity and thus opened a first property in Gurgaon, India. Only two years after its first entry in 2013, OYO Rooms were already expanding to more than 100 cities with a network of over 10,000 rooms and 2,000 hotels.

In 2016, OYO Rooms reached its milestone of over 1 million hotel check-ins, which was followed by the opening of its first Southeast Asian property in Malaysia. Indonesia was its second expansion target in Southeast Asia with the operation of 30 properties and 1,000 rooms recorded by the end of 2018 (Forbes, 2018). However, the company expanded even more aggressively in China a year earlier, with 180,000 franchised rooms and more than 4,000 hotels. OYO Rooms is also leveraging its business by opening OYO Living, supposedly accommodating those of long-term tenancy needs.

ZEN Rooms – Launched in Indonesia, ZEN Rooms is now operating in 6 Southeast Asian countries including Indonesia, Singapore, Malaysia, Thailand, Philippines, and Sri Lanka. ZEN Room was founded in 2015 based on the idea to provide standardized budget accommodations, a segment that was once highly fragmented in Southeast Asia. The startup's business model allows ZEN Rooms to lease some of the rooms from independent property owners, subject to a review and upgrade before marketed under the same brand. The overall occupancy rate of ZEN Rooms in 2017 reached above 90 percent (Straits Times, 2017). As of the beginning of 2017, ZEN Rooms operated 5,000 rooms in Southeast Asia and was about to grow in Singapore with additional 500 rooms.

RedDoorz – Founded in 2015, Singapore's RedDoorz has a network of around 680 properties across 40 cities spread in four Southeast Asian countries, including Indonesia, Singapore, Philippines, and Vietnam. This startup built an online reservation platform for users primarily from Southeast Asia, either for business or leisure (Forbes, 2019). With a 10% increase in the number of tourists visiting at the beginning of 2018, Southeast Asia proved to have the largest growths of any region in the world (United Nations World Tourism Organization, 2018).

RedDoorz see the market as promising ground for such online booking startups. However, there are varying media to which travelers go online to search for accommodations. Indonesia users tend to find the latest travel trends from Instagram, while Facebook is more preferable for Philippines users.

Travelio – Travelio was founded in 2015, about the same time as ZEN Rooms and RedDoorz. But as for Travelio, the operation is still concentrated within the local Indonesian market. It now operates more than 2,000 residential units across 25 cities. Travelio addresses the needs of property owners and consumers for both short-term and long-term rentals with a hotel standard living. Short-term tenants are to be charged by price per night while the long-stay ones are subject to monthly payments.

This startup targets small investors who (1) own multiple vacant homes and bear monthly maintenance cost, (2) invested in residential properties and aim to achieve capital gains on higher resale value, (3) aim to obtain income but do not have the resources to maintain occupancy, manage multiple distribution channels, and logistics (Travelio, 2018).

Impact on the real estate industry

In terms of supply, rental units offered for the short-term are likely to grow in number, particularly in Southeast Asian tourist-destination cities, with Proptech startups providing new affordable hospitality services. Each housing unit reserved for an online accommodation could mean one less unit for long-term residents. By taking supply off the long-term tenancies market, such startups could potentially raise costs (Bloomberg, 2018). Under this assumption, a recent study shows that the impact of owner-occupiers sharing their own properties is rather small on rents, with only a 0.02% rise. However, in the case of commercial operators managing rooms with hotel standards, the effect on market rents is predicted to be bigger (Barron et al., 2018). Proptech startups managing rooms in Southeast Asian countries like OYO Rooms, ZEN Rooms, RedDoorz, and Travelio are reshaping the rental housing landscape by adding more affordable and standardized serviced accommodation into the market. Some startups facilitate not only short-term rentals that are charged per night, but also longer residency commitment with monthly rates. The new Proptech waves in the rental housing market may even fill the absence of affordable serviced apartments. This type of accommodation is to be absorbed by younger executives and families looking for temporary housing options before finding permanent home. Existing supply of serviced apartments in Southeast Asia is typically operated by international hospitality chains offering higher living quality and rental rates while targeting corporate expatriates.

Implications for investors

Through the business model of the reviewed Proptech startups, property investors can benefit from opportunities such as economies of scale typically seen in large hotel chains. Once the investment units are registered, room and service quality are to be improved to meet the startups' standard for operations. Agreements on share revenues are negotiated upfront and room fit outs could either be executed by the property owner or the startup themselves.

More importantly, the Proptech startups could potentially help investors to push up the occupancy rate. In Greater Jakarta, for instance, the cumulative supply of individually owned apartments-for-lease as of Q3 2018 was 117,861 units, many of which were not let due to a lack of marketing efforts (Cushman & Wakefield Indonesia, 2018). In this respect, Southeast Asia can learn from the experience in India, where vacancy rates of short-term rentals decreased by over 10% on average within a month after collaborating with a Proptech startup (Nikkei Asian Review, 2018).

On the other hand, investors should also note the regulations emerging in some of the Southeast Asian countries. Singapore issued a new law prohibiting properties to be rented out for a term less than six months, unless the owner obtained a permission from Singapore's Urban Redevelopment Authority (Urban Redevelopment Authority, 2016). In Malaysia, Penang's Town and Country Planning Act of 1976 plus Trades, Businesses and Industries By-Laws of 1991 were cited for the regulation of any property that is let on a short term is considered as a hotel. Whilst in Vietnam, some residential buildings may have specific rules against short-term leasing.

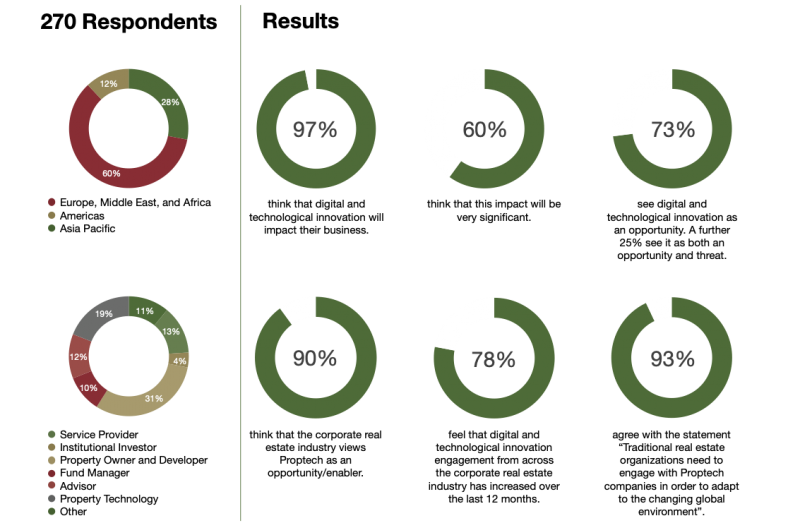

Despite the increased regulations in the rental housing market, most real estate practitioners view Proptech as an opportunity for the property industry. They also agreed that, in order to adapt to the changing global environment, traditional real estate organizations need to engage with Proptech companies. Digital and technological innovation are deemed to give a significant positive impact to the property business (Graph 2 – KPMG, 2018).

Graph 2. The KPMG global proptech survey 2018

Sources

McKinsey Global Institute; Jones Lang LaSalle; Zervas et al.; University of Siena; Asia Green Real Estate; New York Times; CB Insights; Google & Temasek; University of Oxford; Entrepreneur India; Forbes; Straits Times; Forbes; United Nations World Tourism Organization; Travelio; Bloomberg; Barron et al.; Cushman & Wakefield Indonesia; Nikkei Asian Review; Urban Redevelopment Authority; KPMG

Disclaimer

© 2019 Asia Green Real Estate AG, Switzerland. No warranty can be accepted regarding the correctness, accuracy, uptodateness, reliability and completeness of the content of this document. Asia Green Real Estate expressly reserves the right to change, to delete or temporarily not to publish the contents wholly or partly at any time and without giving notice. This document as well as its parts is protected by copyright, and it is not permissible to copy them without prior written consent from Asia Green Real Estate. This material does not take into consideration the specific investment objectives, financial situation or particular needs of any person that enters into a relationship with Asia Green Real Estate. No representation or warranty, expressed or implied, is made by Asia Green Real Estate regarding future performance. This material is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of, or located in, any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or subject Asia Green Real Estate to any registration requirement. The document may contain forward-looking statements that reflect Asia Green Real Estate's current views with respect to, among other things, future events and financial performance. Any forward-looking statement contained in this material is based on our current estimates and expectations and are subject to various risks and uncertainties.

Our complimentary publications inform you about current developments in the Asian real estate market and key trends in the real estate industry. Sign up to receive them automatically.